Potential Impacts of HST on the Construction Industry

Dr Mir F. Ali

This article is a follow up to the article which was posted on the subject of the HST on July 24, 2009.

Unfortunately, at this stage, very little information on the proposed Harmonized Sales Tax (HST) has been provided by the BC provincial government. Transitional rules and other specific details may be released as late as March 2010, leaving almost eight months from the sudden and unexpected announcement of the HST in July until March 2010 for the speculation and only little over three months for the clarification and implementation of the HST. Either this is a direct reflection of the poor planning or overconfidence of the provincial government. Alternatively, it could be a combination of both.

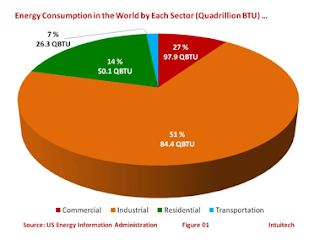

According to a government report, it’s estimated that the HST will remove over $2 billion in costs for B.C. businesses. That includes an estimated $1.9 billion of sales tax removed from business inputs, which enhances competitiveness, increases investment and productivity and, ultimately, increases prosperity. For example, some savings would include about $880 million for the construction industry, $140 million for manufacturing, $210 million for the transportation industry, $140 million for the forestry sector, and $80 million for mining and oil and gas. In addition, B.C. businesses will also save an estimated $150 million annually in compliance costs.

It is hypothesized that the construction industry will be the single biggest beneficiary of the newly-refundable provincial portion of HST. BC Finance estimates that, of the $1.9 billion of PST currently paid by businesses, the construction sector will save $880 million, or 46% of the total expected business savings from conversion to HST.

According to the BC Construction Association Bulletin published on August 06, 2009, commercial real estate customers are the big winners as the provincial portion of HST becomes newly refundable throughout the distribution chain (e.g., forestry, manufacturing, construction) as well as on selling, purchasing and/or rental costs. Here are some observations which were made in an attempt to visualize the impacts of the HST on certain aspects of the construction industry:

Observation 1:

Under the current setup, businesses associated with commercial real estate are entitled to claim or remit their net GST based on its 5 percent. However, under the proposed tax structure, they will pay 12 percent tax (GST 5 + PST 7) on their purchases and collect 12 percent from their customers on their sale, either claiming or remitting the net HST.

Here is an example of the current and the proposed tax structures for purchasing building materials from a wholesale supplier and selling it to a construction company:

| No | Description | Current Tax Structure | Proposed HST Structure |

| PURCHASES | |||

| 1 | Cost for Goods (Building Materials) | $100,000 | $100,000 |

| 2 | GST Paid | $ 5,000 |

|

| 3 | HST Paid |

| $ 12,000 |

|

| TOTAL COST | $105,000 | $ 112,000 |

| SALES | |||

| 1 | Selling Price (Building Materials) | $ 125,000 | $ 125,000 |

| 2 | PST Collected | $ 8,750 |

|

| 3 | GST Collected | $ 6,250 |

|

| 4 | HST Collected |

| $ 15,000 |

|

| TOTAL SALE | $ 140,000 | $ 140,000 |

| Remittances: | |||

| 1 | GST Collected | $ 6,250 |

|

| 2 | GST Paid | $ 5,000 |

|

|

| Net GST (Payable to Federal Govt.) | $ 1,250 |

|

|

| Remittance to Provincial Govt. | $ 8,750 |

|

|

| TOTAL TAX | $ 10,000 |

|

| 1 | HST Collected |

| $ 15,000 |

| 2 | HST Paid |

| $ 12,000 |

|

| Net HST (Payable to Federal Govt.) |

| $ 3,000 |

Similarities and Differences:

-

Under the current sales tax system, goods purchased for resale are PST exempt, therefore, only GST in the amount of $5,000 is payable. GST is fully refundable for the reporting period in which the purchase was made, therefore the TOTAL COST is $100,000. Similarly, under the proposed HST structure, the 12 percent HST will be fully and immediately refunded for a TOTAL COST of $100,000;

-

TOTAL SALE and TOTAL COST are the same under the both tax structures but in case of the current tax system, the amounts for GST ($6,250) and PST ($8,750) are documented and reported separately whereas the amount of HST ($15,000) will be calculated and remitted together to one taxation authority and potentially subject to only one audit review;

-

Under the current sales tax system, the combined tax remitted by the business is $10,000 (after deducting the GST input tax credit of $5000) whereas the net amount to be remitted under HST will be $3,000, i.e., $15,000 - $12,000;

-

Under HST, the business’ supplier will collect and remit $12,000 on its sale of materials to the business whereas the net amount to be collected and remitted under GST was only $5,000; and

-

There may be a timing difference, i.e., a positive or negative cash flow effect depending upon whether the business must remit the net GST or the net HST to the government on its sales before or after it pays the tax to its suppliers on credit purchases.

This is the most pure example of “revenue neutral” under the proposed HST.

Observation 2:

Contrary to the popular belief that no changes are applied to homes for $400,000 and under, here is an example of a new home:

| No | Description | Amount | |

| PURCHASE PRICE: | |||

| 1 | Price of a Home | $ 350,000 | |

| 2 | Applicable HST | $ 42,000 | |

|

| Sub-Total | $ 392,000 | |

| APPLICABLE REBATES: | |||

| 1 | Less GST Rebate | -$ 6,300 | |

| 2 | Less Provincial HST Rebate | -$ 17,500 | |

|

| Sub-Total | -$ 23,800 | |

|

| Net Cost | $ 368,200 | |

| PAYABLE TO CRA: | |||

| 1 | Amount to be remitted | $ 18,200 | |

Here is an explanation:

-

Applicable HST is based on 12 percent of the price of the home;

-

Less GST Rebate is calculated “36 percent of 5 percent rebate” and the formula is:

-

(Price of a home*5/100)*36/100

-

-

Less Provincial HST Rebate is calculate 5 percent of the price of the home; and

-

Amount to be remitted to CRA is calculated by subtracting Price of the Home from Net Cost.

However, under HST, the developer will not pay PST on the cost of construction. Construction Cost (Building Materials, etc.) in this example is $200,000, the developer is required under the current setup to pay $14,000 PST on the construction cost, plus net GST of $11,200 (net 3.2% x $350,000). In other words, the developer is getting a break under HST.

Observation 3:

There are a number of grey areas that need to be addressed but based on the information available for the homes priced above the threshold of $400,000; the following example will illustrate how much more a consumer will have to pay for purchasing a new home under the proposed HST:

| No | Description | Amount |

| PURCHASE PRICE: | ||

| 1 | Price of a Home | $ 500,000 |

| 2 | 12% HST | $ 60,000 |

| APPLICABLE REBATES: | ||

| 3 | Minus Rebate | -$ 20,000 |

| 4 | Embedded PST Credit 2% on price | -$ 10,000 |

|

| TOTAL REBATES | -$ 30,000 |

| 5 | HST After Rebates | $ 30,000 |

| 6 | Current 5% GST | $ 25,000 |

| 7 | Increased Tax | $ 5,000 |

|

| Percentage of Increase | 1.00% |

Here is an explanation:

-

A rebate of $20,000 is offered to minimize the amount of HST regardless of the size of the price of a home;

-

The other tool that the government is offering to reduce the impact of the tax is the Embedded PST Input Credits. While government press releases indicate the input credit will be approximately 2.5 percent, some reliable sources indicate it is more likely 2.0 percent or less. Therefore the amount of $10,000 calculated based on a 2 percent credit;

-

When the combination of a rebate and the embedded PST credit is applied against the applicable HST, the HST amount is shown as $30,000;

-

The result of the comparison between the calculated GST under the current setup with the proposed HST setup shows that the consumer will pay $5,000 more under the proposed HST for purchasing a home for $500,000 which represents 1 percent; and

-

The amount of difference grows as the price of the home increases. For instance, in case of a home with the price of $600,000, the difference grows to $10,000 which represents 1.67 percent increase whereas in case of a home with the price of $1,000,000, the difference grows to $30,000 which represents 3 percent increase.

Urban Development Institute (UDI), Pacific Region, forwarded the following recommendations to the Premier in Response to the New HST:

-

Significantly increase the $400,000 threshold in the growth areas of the Province – Vancouver, Victoria and Kelowna. Greater Vancouver house prices are the highest in the country;

-

Index the threshold, so it increases as housing prices rise;

-

Increase the maximum rebate in growth areas to reflect higher housing costs in these areas;

-

Grandfather pre-sale contracts written before July 1, 2010 (even if ownership and the transfer of title occurs after this date);

-

For housing units that are completed but not pre-sold or those that need to be self assessed for rental purposes, ensure that any PST obligation which occurs before July 1, 2010 can be offset against HST, irrespective of the date of sale or self assessment of units; and

-

Further discussion is needed to review and mitigate the impact of the HST on rental housing; specifically, self supply assessment on new purpose built units and the lack of flow through of HST charges on services (e.g. landscaping, janitorial, and property management) from landlords to renters under the Residential Tenancy Act on new and existing rental units.

It is clear from the information presented in this article that consumers are going to end up paying more tax under HST but the developers and builders are going to get a break for not having to pay PST on the construction cost which will help boost the economy. At the same time, there is a strong possibility that the developers and builders are going to consider giving consumers a break by subsidizing the additional tax on new homes. Carl Beck in his article published in the BC Construction Association made his point that market forces will have much more of an effect on the price of new homes, resale homes and construction services than any form of taxation.

———————

The examples presented in this article were vetted by Carl Beck, CMA, Sales Tax Advisor. Carl Beck has extensive experience advising clients during sales tax transitions, having been directly involved in the implementation of GST in 1991, Quebec Sales Tax (QST) in 1995 and HST in the Maritimes in 1997 (carl.beck@telus.net)

Comments